Research Survey on Interest Limitation in China/Shen Siqi

- S Chen

.jpg/v1/fill/w_320,h_320/file.jpg)

- Jan 28, 2025

- 2 min read

Updated: Mar 28, 2025

Research Survey on Interest Limitation in China

Student name: Shen Siqi

The research on interest deduction limitation rules in China is mainly embodied in the management of thin capitalization which aims to limit the interest deduction between related parties (including enterprises, shareholders and other related individuals).

Compared with other countries in the world, China's thin capitalization system started a little late, and the relevant thin capitalization provisions were formally introduced into domestic laws and regulations only in 2008, when the “Corporate Income Tax Law”, its “Implementation Regulations” and “Measures for the Implementation of Special Tax Adjustments (Trial)” came into force in China, establishing the anti-avoidance framework of China's corporate income tax based on international practices. In 2011, the first tax avoidance case of a Japanese enterprise in Shaanxi, which utilized interest deduction for related loans, was investigated and sanctioned, and the tax amount was as high as 30 million yuan after a special tax adjustment by the tax department, and the enterprise paid a tax reimbursement of more than 11 million yuan.

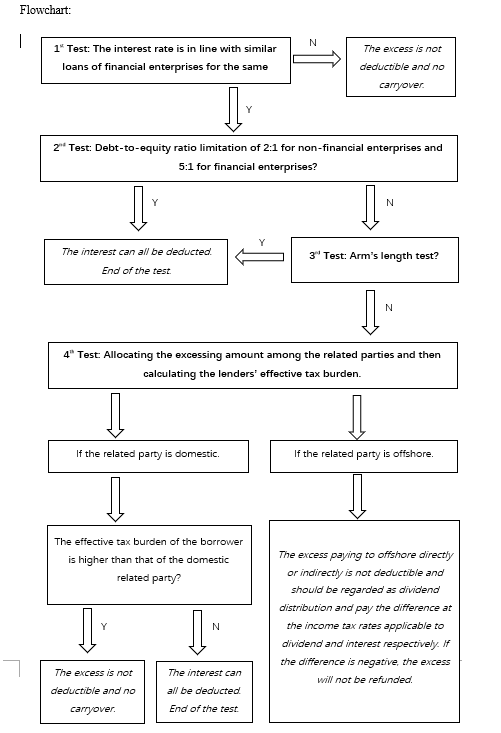

The general principle of thin capitalization in China is based on the fixed ratio and arm's length transactions and will be subject to up to four tests as follows (see the flowchart on the last page).

The first test is to comply with the interest rate of similar loans of financial enterprises for the same period of time and the excess is not allowed as a deduction.

After passing the first test, the second test, the fixed ratio test, is performed, which requires a 5:1 ratio of debt-to-equity investment if the borrower is a financial enterprise, or a fixed ratio of 2:1 if the borrower is a non-financial enterprise, with interest expense allowed as a deduction to the extent below the ratio.

The excessing amount of the second test is subject to the arm's length principle, the third test, and if it passes the test, the excess is allowed.

If the third test is not passed, the excessing in the 2nd test needs to be allocated among the related parties, and based on the result of the allocation before entering into the fourth test, the enterprise's effective tax burden test. If the effective tax burden of the borrower enterprise is not higher than that of the domestic-related party, the excess is allowed to be deducted; if it is higher than that of the domestic-related party or is paid directly or indirectly to the foreign-related party, the excess is not allowed to be deducted and for the outbound part, it should be regarded as dividend distribution and subject to Corporate Income Tax (hereinafter as “CIT”) according to the difference in the income tax rates applicable to the dividend and the interest, respectively. Besides, if the amount of withholding tax more than the amount of CIT payable on the basis of dividend, the excess will not be refunded.

One thing to be clear is that there is no carryover if the interest payment is justified as non-deductible.

63

Comments